As Project Managers, managing construction project budgets might not be the sexiest part of our job description, but we should be more proud of the skill required for this craft, and here is why: it isn’t just “peanut counting” it is an art that requires finesse and expertise. Sure, in order to manage a budget well, you must have an understanding of how to track numbers, but more importantly, you must understand you are painting a picture and telling a story with those numbers. You must utilize your creativity, vision, and a delicate touch of when or how to incorporate the numbers to ensure the picture you are painting is an accurate reflection not only of where the project financials stands in this moment, but also where they will stand at some point in the future.

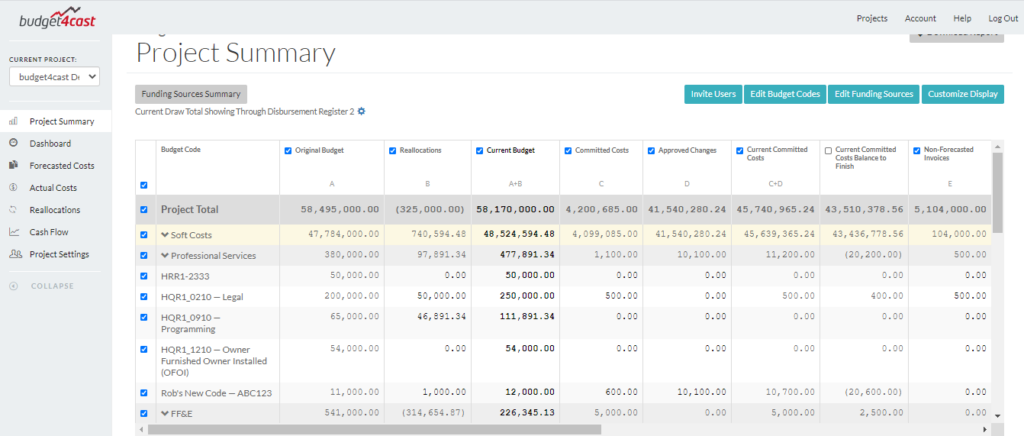

When we are successful, the resulting picture that a properly managed project budget should paint is one with a lot of depth. However, I think many of us are only achieving a level of budget management that is elementary, maybe closer to “painting by numbers” rather than painting a masterpiece with numbers. Too often we are content to simply account for the costs spent to date and track them against the original budget amount. When we do this we are leaving so much depth out of our picture, depth that our stakeholders want and need to see. The key for creating a budget masterpiece with depth that speaks to our stakeholders is in utilizing forecasted costs.

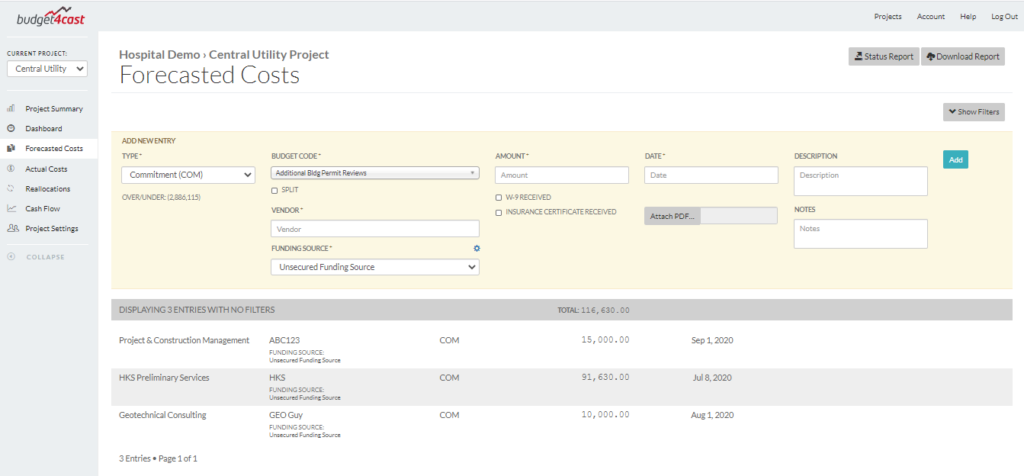

Forecasted costs come in a couple of different types: Commitments (or contracts), Potential Changes, Approved Changes, and Uncommitted Costs.

Tracking Committed Costs and Approved Changes are an easy way to add dimension to your project budget picture. When you have a contract, proposal, or any type of agreement to pay someone an amount in the future, that is a Commitment. Any subsequent change to that Commitment that has been approved is an Approved Change. When you track those events against a budget line they will automatically forecast the total you anticipate spending against that budget line. This adds a lot of depth to the picture because it starts to account for not only what has been spent to date, but also what we anticipate will be incurred and therefore where we will end up at the end of the project.

Potential Changes come from any event or possible event we as project managers foresee taking place that could result in an increase or decrease to one of the Committed Costs. The artistic skill required in handling these costs is rooted in accurately projecting what the cost may be and when to start including those costs in your forecasting. If you’re too quick to track potential changes and too conservative in estimating the costs, you’ll very quickly paint a picture of construction project budget overruns and project chaos. However, not all potential changes turn into real changes and not all estimated costs will be the actual costs incurred, so a delicate hand is needed to properly include these items without ruining the picture. One way is to include new Potential Change line items in your budget projection as soon as you are aware of them, but wait to include costs on those lines until you have a confident estimate from yourself and/or a third party. This way the picture of your budget at any given time will suggest to the viewer there are potential costs looming, but they won’t be painted in such bold lines that they dominate the entire image of the construction project budget.

That leaves us Uncommitted costs. Uncommitted costs are placeholders for future costs the manager thinks will be incurred, but are not yet Committed.

If you include too few Uncommitted placeholders, you’ll be painting a picture of a project that will wrap up well under budget (when in fact it may just be that those future costs have not yet been Committed but you know they will be at some time in the future and so an entire budget line will be spent). Infrequent adjustment to Uncommitted Costs or overly conservative estimates of Uncommitted Cost amounts will show a project heading well over budget (when in fact those costs may not materialize, or may have already materialized in the form of a Commitment or Approved Change you already included). Uncommitted Costs should typically be numerous at the beginning of a construction project and then diminish as a project proceeds because they are being turned into Commitments or Approved Changes. You could think of them as a pencil outline of shapes in your picture that hold the place of where something is going to be painted. As the painting proceeds you’ll paint over the pencil and make that placeholder permanent, or you’ll erase the image to make room for a new shape. Uncommitted costs should be converted into Commitments (painted over), or removed (erased) as a project progresses.

By working with forecasted costs and recognizing they are our opportunity to paint a picture with our numbers, we can create a masterpiece to share with our stakeholders, and they’ll thank us for it.

To learn more about construction project budget forecasting and check out a tool that will make you the Bob Ross of budgets, check out our website.